Loading ...

Loading...

Loading ...

The Opening Range Breakout (ORB) is one of the most popular intraday strategies among professional day traders. It's based on a simple hypothesis: the high and low of the first few minutes of trading often set the tone for the rest of the day. When price breaks through those levels, it tends to continue in that direction.

For 0DTE options traders, the ORB takes on special significance. The explosion of daily SPX expirations since 2022 — with 0DTE volume now accounting for a massive share of total SPX options activity — has created structural market dynamics that can reinforce opening range levels. Market maker hedging flows, gamma exposure, and concentrated single-session volume all contribute to making the opening range a meaningful reference point for the trading day.

But here's the catch: not all ORB setups are created equal. The choice of range duration, entry style, position type, and the filters you layer on top can mean the difference between a robust edge and a strategy that bleeds money on false breakouts. The only way to know what works is rigorous backtesting.

In this guide, we'll explain how the ORB strategy works, what the trading community has learned about it, and how to backtest it on SPX 0DTE options using GreeksLab — visually, without writing a single line of code.

The opening range is the price range (high and low) established during the first N minutes of the trading session. Common durations are 5, 10, 15, 30, or 60 minutes.

A breakout occurs when the underlying price moves beyond this range:

The theory is straightforward: the opening range captures the initial battle between buyers and sellers. The open is the most active period of the trading day, with institutional orders, overnight positioning, and economic data reactions all concentrated into a narrow window. When one side wins decisively enough to push price beyond that range, it signals a directional move worth trading.

0DTE options are uniquely suited for the Opening Range Breakout for several reasons:

The trading community has converged on two primary approaches for combining ORB with 0DTE options:

1. Directional Buying (Long Calls or Puts)

When price breaks above the opening range high, buy a call. When it breaks below the low, buy a put. This approach typically has a lower win rate but relies on winners being significantly larger than losers. The extreme gamma of 0DTE options means a genuine breakout can cause an option to double or more in value on a moderate underlying move, while your maximum loss is capped at the premium paid.

Shorter opening range durations provide earlier entries and more trading time for the position to develop, while longer durations may offer more reliable signals. Both are worth testing.

2. Credit Spreads (Premium Selling)

Instead of betting on continuation, this approach sells credit spreads that profit from the market staying on the right side of the opening range. When price breaks above the opening range high, you sell a put spread below the range low (betting the low will hold as support). When it breaks below the low, you sell a call spread above the range high.

This approach typically produces higher win rates but with an asymmetric risk profile: each win collects a relatively small premium, while losses can be significantly larger. Some traders prefer longer opening range durations for credit spreads, reasoning that the range levels are more established, but the ideal duration depends on the specific setup and market conditions.

Both approaches are worth backtesting. GreeksLab supports building either one.

The choice of opening range duration is not just a minor tweak — it can dramatically change performance characteristics. Each duration has distinct tradeoffs:

There's no universally "best" duration — it depends on your position type, risk tolerance, and market conditions. This is exactly why backtesting matters.

The single biggest challenge with ORB strategies is the false breakout: price briefly pokes above the range high (or below the low), triggers your entry, then reverses back into the range. ORB traders have developed several filters to address this — each worth testing independently:

Different days of the week have different structural characteristics that may affect ORB performance:

Whether these effects matter for your specific ORB configuration is an empirical question. GreeksLab's Day of the Week condition makes it easy to test each day separately or exclude specific days to see if it changes your results.

The volatility environment changes how ORB strategies behave, and different VIX levels create different conditions:

How your specific ORB configuration performs across these regimes is worth testing. GreeksLab's VIX Price or Underlying ATM Straddle Premium conditions let you filter entries by volatility level to see how it affects your results.

How the market opens relative to the previous close may affect the ORB setup. Large gap days — where SPX opens significantly higher or lower than yesterday's close — create different conditions than flat opens. Some traders believe large gaps "use up" directional energy, while others see them as momentum confirmation.

Rather than assuming which is better, test it. GreeksLab's Underlying Gap condition allows you to filter by gap size, or create separate strategies for gap vs. no-gap days to see how your ORB performs in each scenario.

A key risk when backtesting Opening Range Breakout or any other strategy is overfitting — tuning parameters to fit historical data so precisely that the strategy fails on new data. With ORB, the temptation is to stack multiple filters (VIX range, day-of-week exclusion, gap filter, minimum width, breakout buffer) all optimized to the same historical period.

A more reliable approach: test each filter independently to understand its impact, then combine only those that each showed improvement on their own. If a filter only marginally improves results, it may not be worth the added complexity.

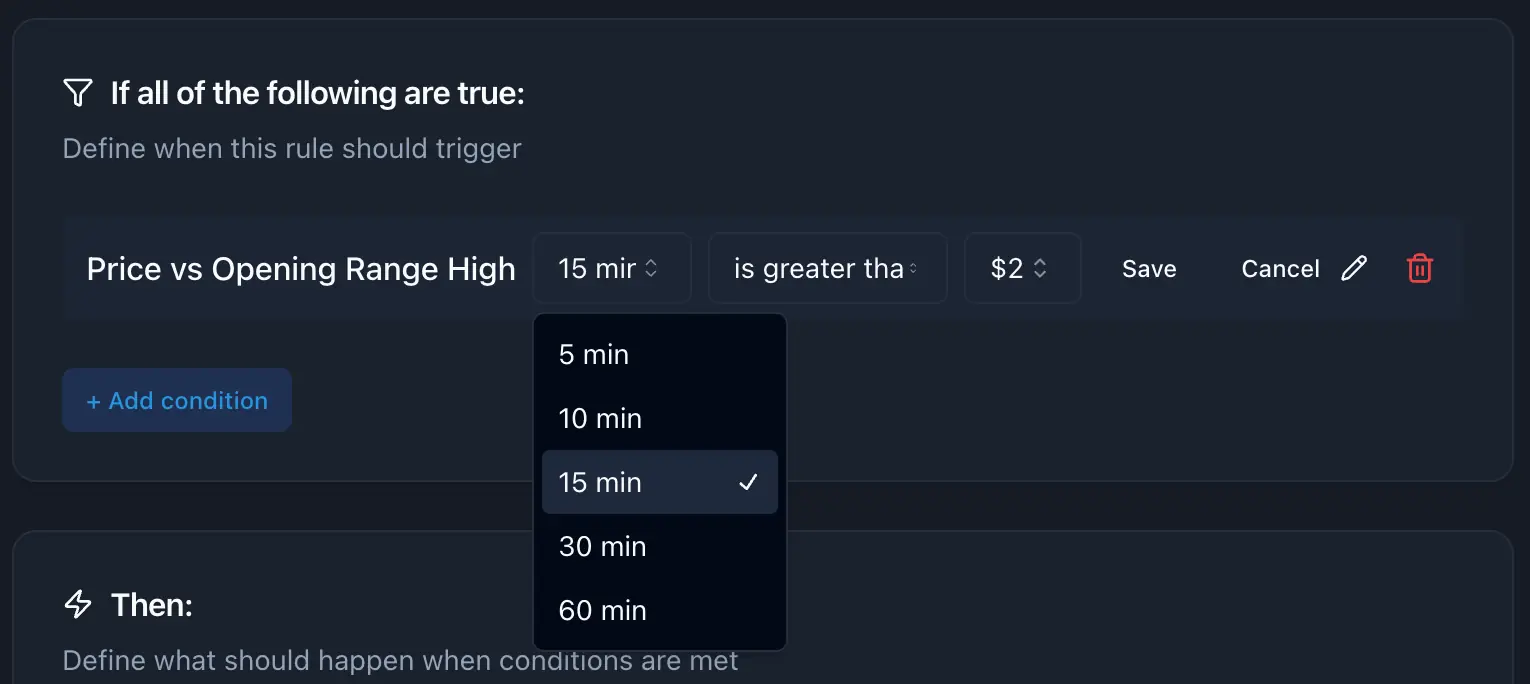

GreeksLab's condition system includes Price vs Opening Range High and Price vs Opening Range Low conditions that make this strategy straightforward to test. Here's how to set it up step by step.

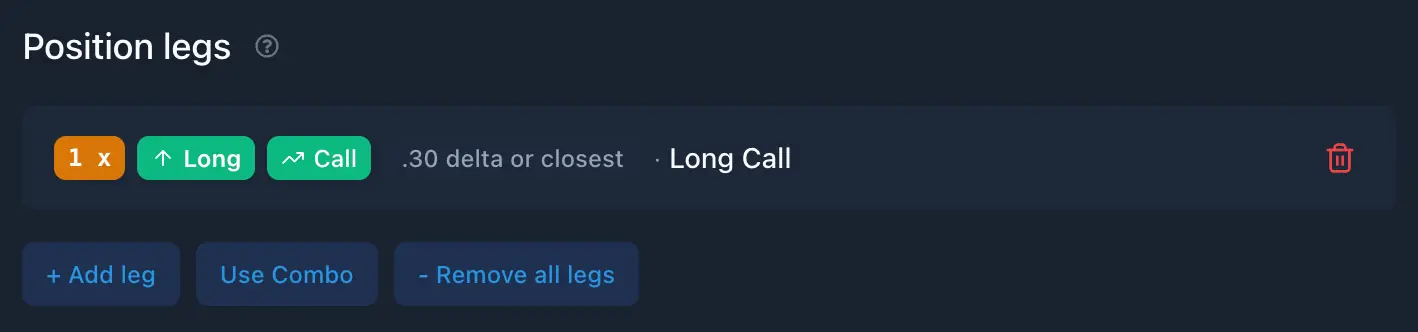

Configure what you want to trade when the breakout signal fires.

For directional buying:

For credit spreads:

In your Entry Rules:

You'll see a duration dropdown where you can select the opening range period: 5 min, 10 min, 15 min, 30 min, or 60 min.

Set the condition to:

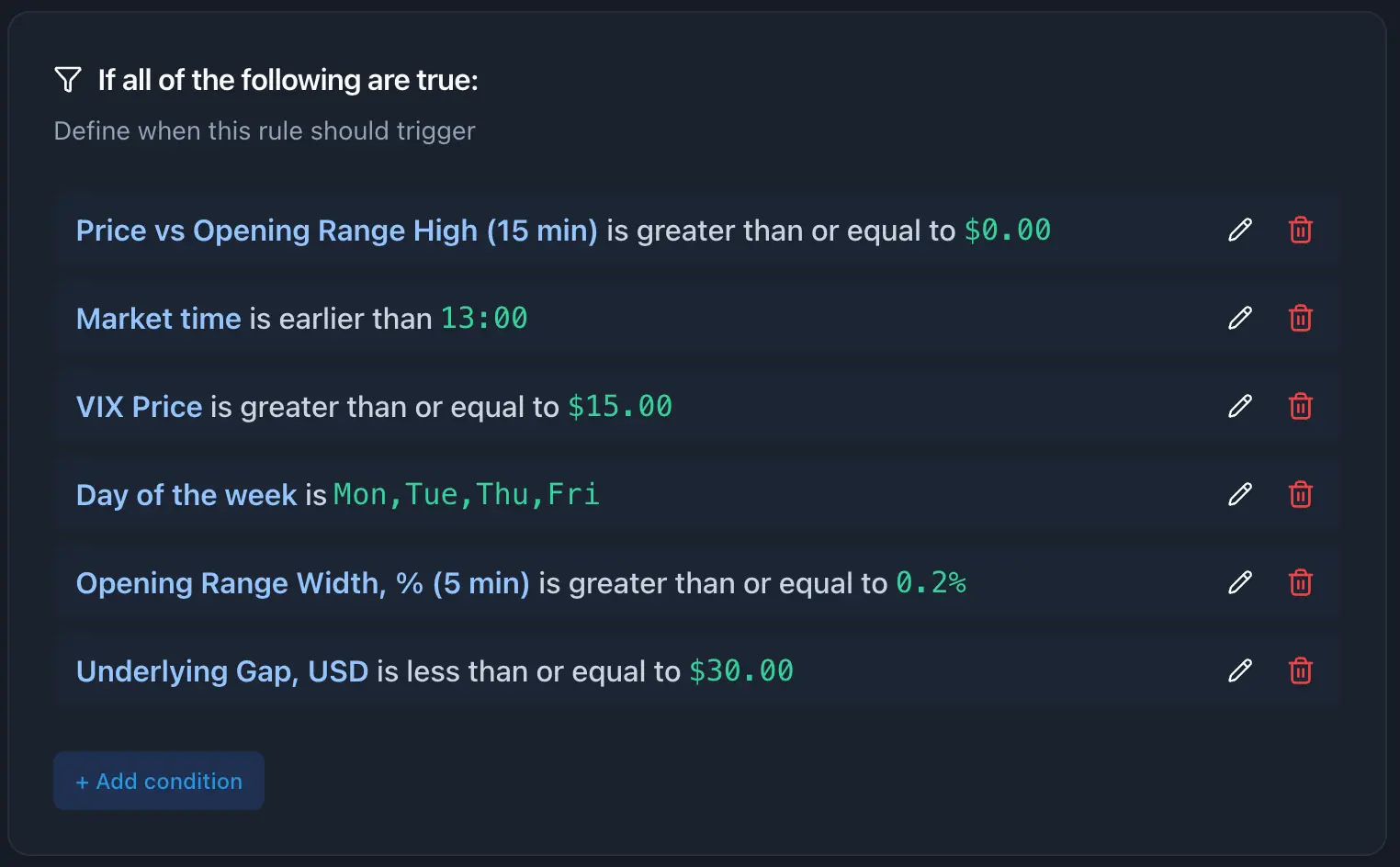

Price vs Opening Range High (15 min) is greater than or equal to $0

This means: "Enter when the current SPX price is at or above the 15-minute opening range high."

To add a breakout buffer that filters weak breakouts, increase the value:

Price vs Opening Range High (15 min) is greater than or equal to $2

Now price must move at least $2 beyond the range boundary before entry triggers.

You can layer on additional filters to refine your entry signal. For example:

Time filter — Control when entries can happen:

Time is earlier than 13:00

VIX filter — Filter by volatility regime:

VIX Price is greater than or equal to $15

Day of week filter — Exclude structurally difficult days:

Day of the Week is not Wednesday (or whichever days your backtesting reveals as weak)

Minimum range width filter — Require a meaningful range size:

Opening Range Width, % (15 min) is greater than or equal to 0.2%

Or use the USD version if you prefer an absolute threshold:

Opening Range Width (15 min) is greater than or equal to $10

Gap filter — Skip days where a large gap may undermine the setup:

Underlying Gap, USD is less than or equal to $30 (absolute value)

GreeksLab combines multiple conditions with AND logic, so all filters must be satisfied for entry.

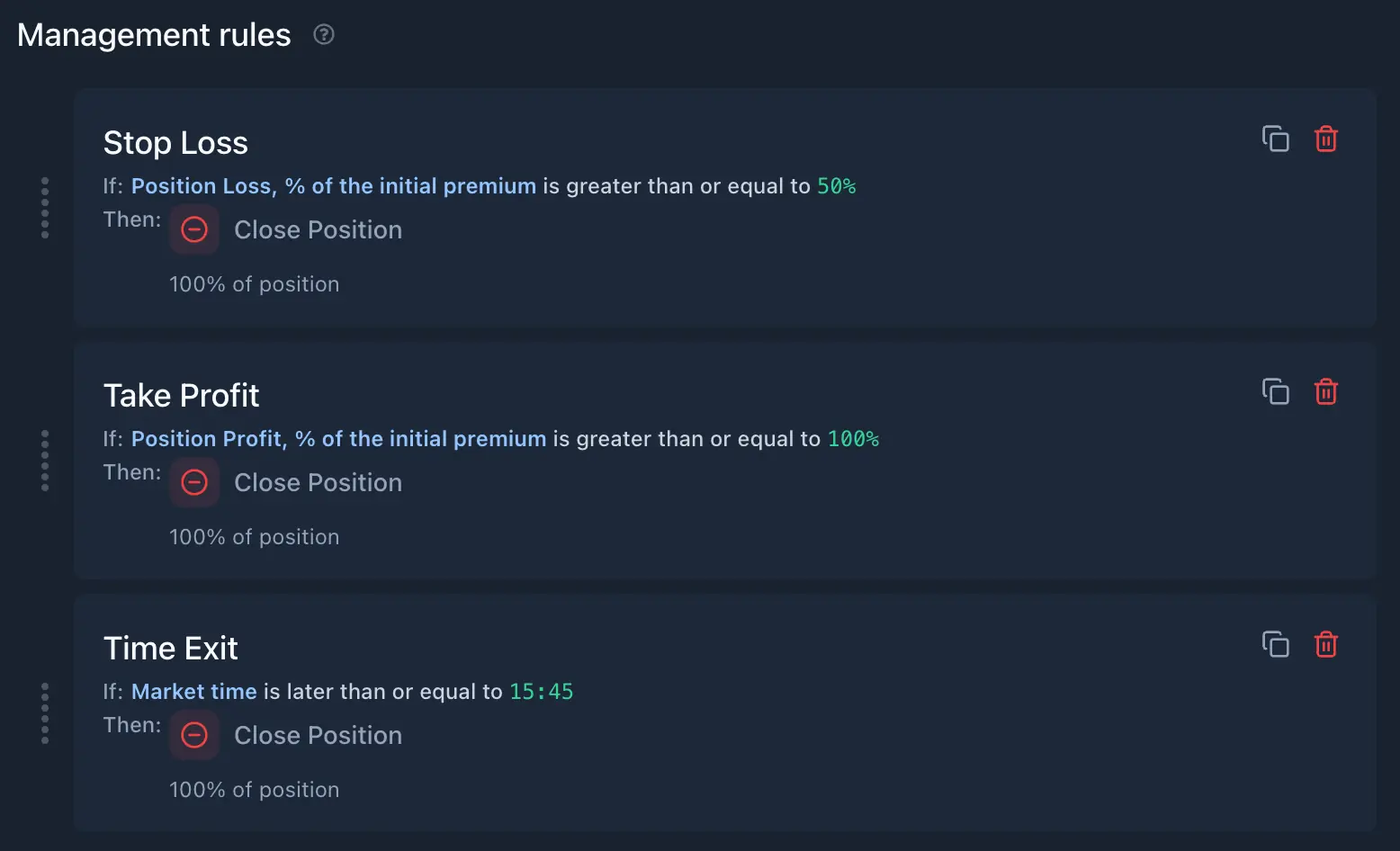

Every good strategy needs defined exits. Add management rules for:

Profit Target:

Stop Loss:

End of Day:

For credit spread strategies, you may choose to hold until expiration to capture full theta decay, using only a stop loss and EOD exit.

Rather than trying to optimize everything at once, take a systematic approach:

Start with a simple configuration — a single duration, no filters beyond a time cutoff, standard profit target and stop loss. This gives you a baseline to measure improvements against.

Create separate strategies for each duration (5, 10, 15, 30, 60 min) with identical parameters otherwise. Use GreeksLab's Compare feature to see them side by side. Look for which durations produce the best risk-adjusted returns, not just the highest total return.

Test each filter independently against your best-performing baseline:

Only combine filters that each independently showed improvement. Don't stack four optimized filters together and assume the combined result is reliable.

Run your final strategy for bullish breakouts and bearish breakouts separately. Check whether one direction is significantly stronger than the other. If both are profitable, consider whether combining them in a portfolio improves risk-adjusted returns.

If you've been testing with long options, try the same ORB signal with credit spreads (or vice versa). The same entry signal can produce very different results depending on the position type.

After running a backtest, focus on these key metrics:

Be cautious if you see:

Once you have several ORB variations backtested, use GreeksLab's Compare feature:

The correlation matrix is especially valuable. If your bull and bear ORB strategies have low or negative correlation, combining them can smooth your equity curve significantly. Similarly, combining a short-duration aggressive strategy with a long-duration conservative one may produce better risk-adjusted returns than either alone.

Use the Combine feature to see what a portfolio of ORB strategies would look like with different weight allocations.

The Opening Range Breakout is one of the most widely discussed intraday strategies in trading, and the growth of 0DTE options has given it new relevance. The structural market dynamics created by concentrated same-day options volume may reinforce opening range levels in ways that didn't exist before 2022.

Whether ORB works for your specific setup depends on many factors: duration, position type, market conditions, and the filters you apply. The only way to find out is to test it systematically.

With GreeksLab, you can:

The key to success is systematic exploration and honest analysis. Backtest, compare, filter for robustness, and let the data guide your decisions.

Ready to test your Opening Range Breakout strategy? Sign up for GreeksLab and start backtesting today.

Create a free account or sign in to access: