Loading ...

Loading...

Loading ...

We looked at 32 Federal Open Market Committee (FOMC) decision days — June 2022 through April 2026 — and measured each one minute by minute against the roughly 970 normal 0DTE days around it. This post reports what happened to the size of the move, to option premium, and to a set of short-premium strategies traded on those days.

0DTE (zero-days-to-expiration) options expire the same day they are traded. On an FOMC day the rate decision is released at 2:00pm ET and the press conference follows, so a scheduled, market-moving event sits inside the 0DTE trading session. Thirty-two meetings is a modest sample, so the numbers below are observations, not rules.

On a normal session, a 0DTE option loses theta — the time-value portion of its price — steadily from the open to the close, because the option resolves to its intrinsic value by 4:00pm and the clock runs the whole way. See How IV Moves Intraday for the intraday mechanics.

A Fed day interrupts that decay. With a market-moving decision scheduled for 2:00pm, sellers hold time value in the options ahead of the announcement. Implied volatility (IV — the expected movement priced into an option) and the dollar premium stay elevated through the morning, then drop once the decision is out. That drop is IV crush. The rest of this post measures it. VIX, VIX1D, and the Term Structure covers how the event premium appears in the volatility indices.

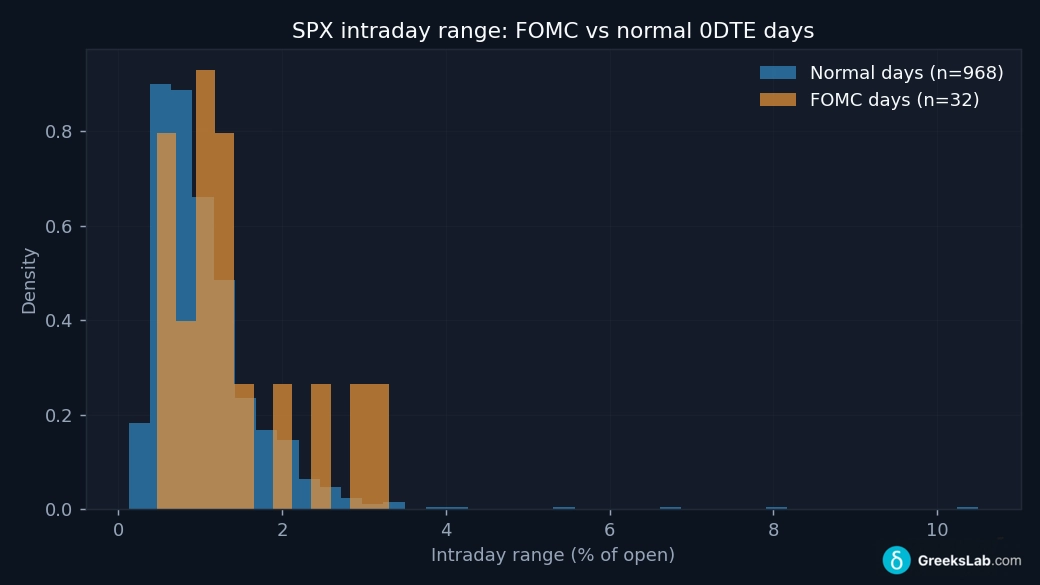

Fed days are wider than normal days, and the difference is concentrated after 2:00pm.

Across the 32 meetings, SPX's average intraday range was 1.41% of price, versus 1.05% on a normal day. The gap is largest after the announcement: the average range from 2:00pm to the close was 1.30% on Fed days, against 0.46% on normal days — about 2.8 times wider.

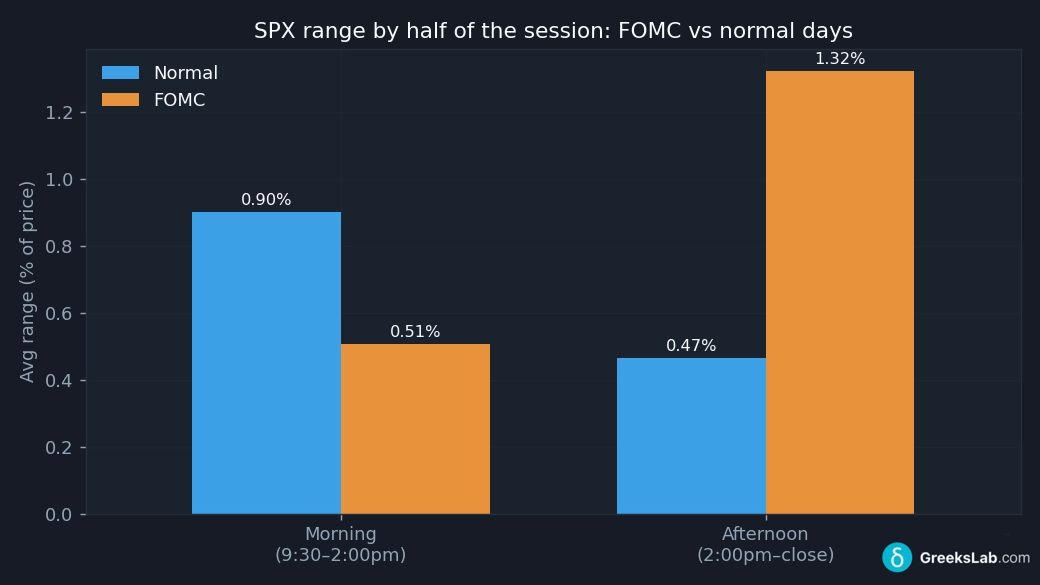

Splitting the session in half makes the pattern clearer. A Fed-day morning is actually quieter than a normal morning — a 0.51% range versus 0.90% — as the market coils ahead of the decision. Then nearly all of the movement arrives in the final two hours.

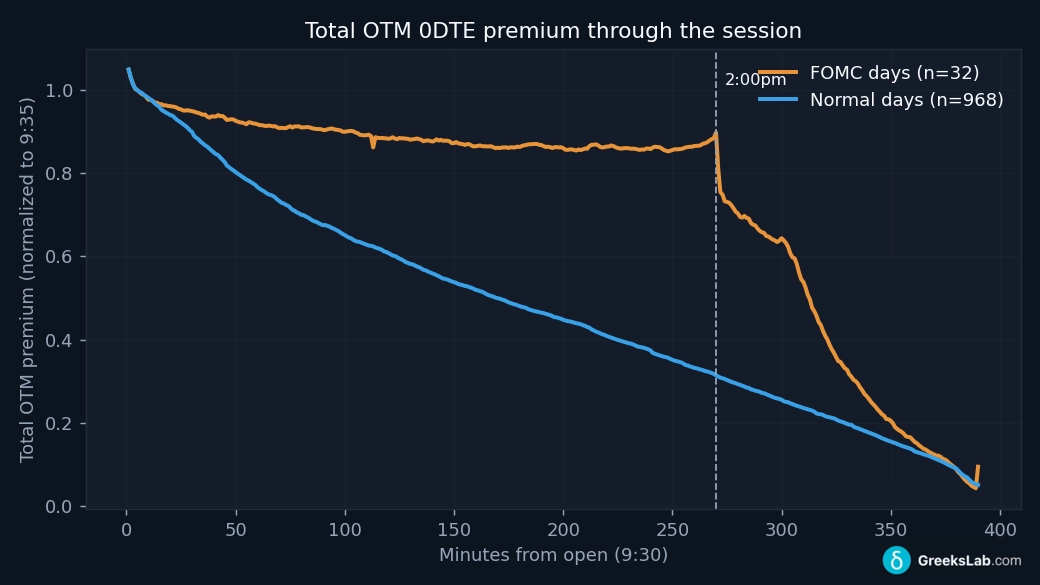

The clearest measure is the total premium in all out-of-the-money (OTM) options on the board — every call above the current price and every put below it. It is a single figure for how much time value is available to a seller.

Each day is normalized to its 9:35am level so days of different size compare fairly. On a normal day, the premium declines steadily all session — ordinary theta decay. On a Fed day, it holds nearly flat through the morning, stays elevated into the 2:00pm line, then drops sharply.

In dollar terms, just before the announcement the total OTM premium on a Fed day averaged about $281, versus $55 on a normal day — roughly 5.1 times higher. In the 15 minutes after 2:00pm it fell 27.9%, against 20.8% over the same window on a normal day. That is the event being priced out of the options.

IV moves the same way directionally. We report the dollar figure rather than IV because a 0DTE option's annualized IV is distorted as expiration approaches and the time-to-expiry term shrinks toward zero, which makes the raw premium the cleaner measure.

This cuts two ways, depending on which side of the premium you are on.

A seller collects that inflated premium up front, and the crush is what hands it back as profit. An option sold for a rich price into 2:00pm is worth far less an hour after the announcement, and the seller keeps the difference — as long as the actual move stays smaller than the premium they took in.

The timing works differently from a normal day, though. Because the premium holds flat through the morning instead of bleeding lower, an early entry earns almost nothing until 2:00pm — there is no steady morning theta to collect, only the entry credit sitting unrealized while the position waits for the event. The profit arrives in the crush after the announcement, not gradually through the session. That is why, in the backtest further down, morning entries took five to six hours to reach their profit target while entries placed just before 2:00pm got there in under an hour. The larger, more durable premium means more to collect, but it is mostly collected in the half hour after 2:00pm. The risk a seller carries is the size of the move, not the passage of time.

A buyer pays that same inflated premium, and the crush works against them. Being right on direction is not enough. The post-2:00pm move has to be large enough to cover both the elevated price paid at entry and the drop in implied volatility that follows the decision. A move that would have profited on a normal day can still lose on a Fed day, because the option cost more to buy and a chunk of its value evaporated the moment the uncertainty resolved. That is the same crush in the chart above, seen from the other side.

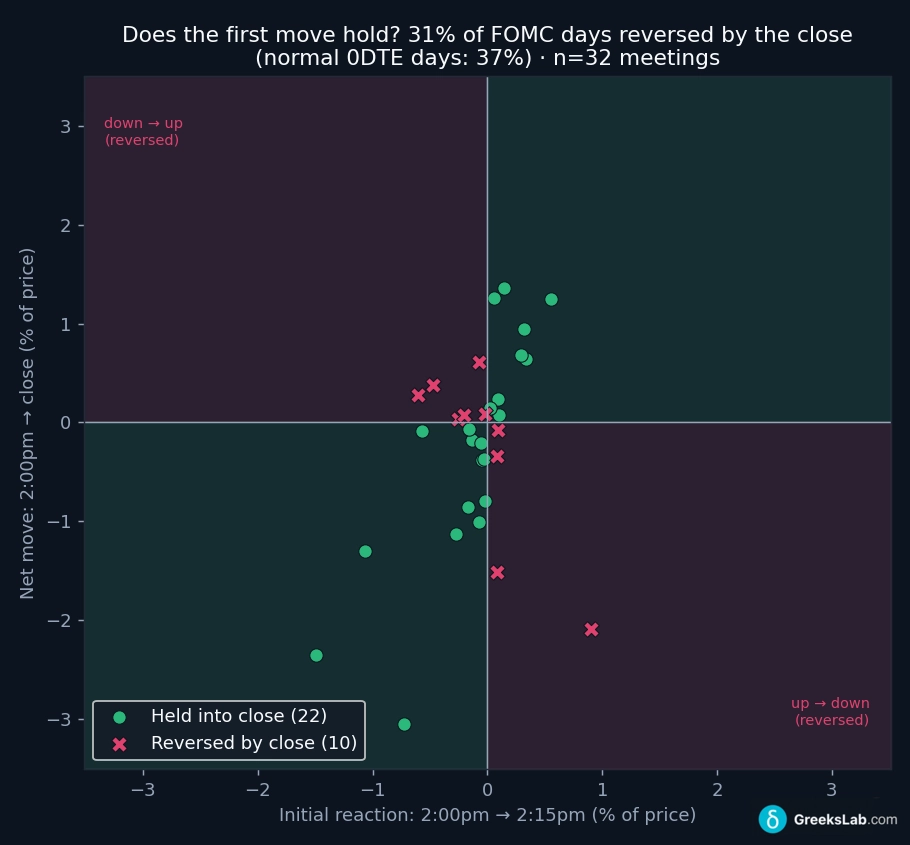

A common claim is that the initial reaction to the FOMC statement reverses later in the afternoon. We measured it.

For each meeting we took the direction of the move from 2:00pm to about 2:15pm, then checked whether price closed on the opposite side of its 2:00pm level. Across the 32 days, the initial move reversed by the close 31% of the time. On normal days the reversal rate was 37%.

Each point is one meeting: the horizontal axis is the initial reaction (2:00pm→2:15pm), the vertical axis is the net move to the close. Points in the green quadrants held their direction; the ten in the red quadrants reversed.

The initial post-2:00pm move therefore held into the close about 69% of the time on Fed days — more often than on normal days, not less. With 32 observations this is a tendency rather than a settled result.

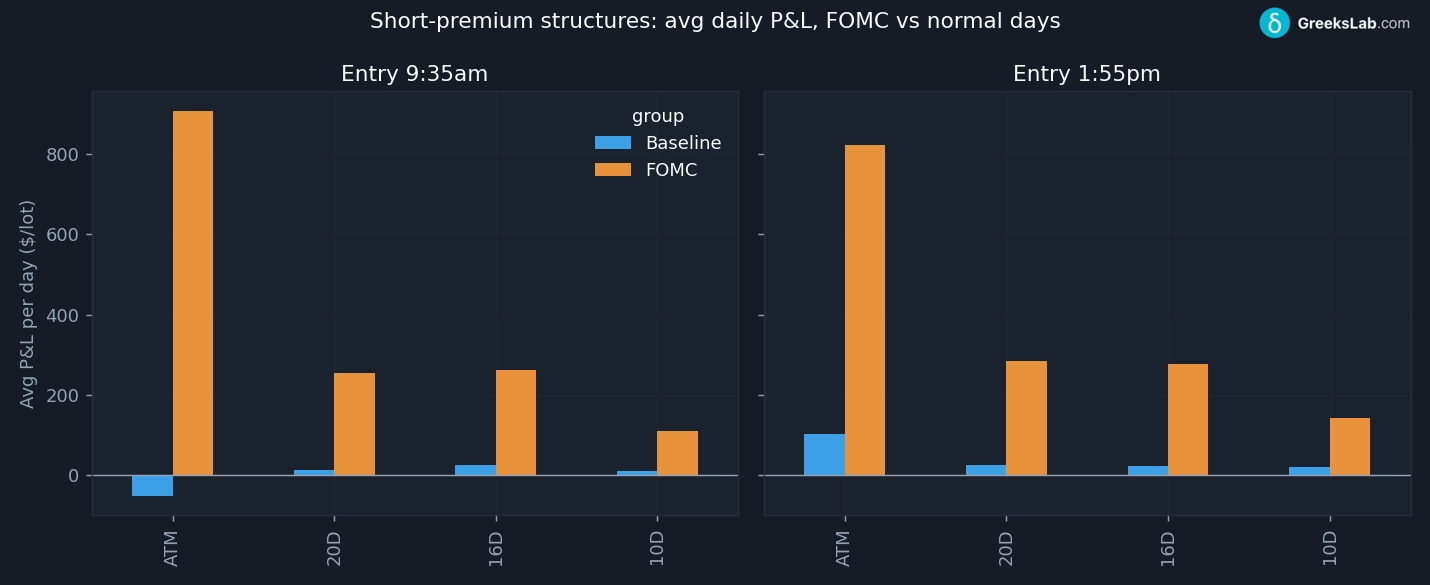

We ran four short-premium structures, entered on every day in the period and managed the same way — take profit at 50% of the credit collected, stop at a 100% loss — then split the results into Fed days and normal days.

We tested two entry times: 9:35am (held all day) and 1:55pm (entered just before the decision).

The chart shows the average daily P&L for all eight configurations on Fed days (orange) against the same trades on normal days (blue). The table below gives the full Fed-day detail, per contract, across the 32 meetings:

| Structure | Entry | Win rate | Avg P&L / day | Worst day |

|---|---|---|---|---|

| ATM straddle | 9:35 | 69% | +$908 | −$3,947 |

| ATM straddle | 1:55 | 66% | +$824 | −$2,743 |

| 20Δ strangle | 9:35 | 78% | +$256 | −$1,450 |

| 20Δ strangle | 1:55 | 81% | +$286 | −$1,660 |

| 16Δ strangle | 9:35 | 81% | +$263 | −$1,117 |

| 16Δ strangle | 1:55 | 84% | +$278 | −$1,145 |

| 10Δ strangle | 9:35 | 78% | +$110 | −$649 |

| 10Δ strangle | 1:55 | 84% | +$143 | −$632 |

Three results:

Every structure earned more per day on Fed days than on normal days. The elevated premium is sold and then crushed, and the seller keeps the difference.

The at-the-money straddle had the highest average and the largest losses. It averaged about $908 per contract per day at a 69% win rate, with a worst Fed day of −$3,947 — more than four times a typical winner. Moving further OTM reduced both the average and the worst day in step: the 10-delta strangle averaged about $110–143 per day with a worst day near −$640. See Naked Short Calls and Short Puts on 0DTE and Straddles and Strangles.

The edge was specific to Fed days. Selling the same ATM straddle at the open on normal days lost money over the period: −$51 per day on average, −$49,737 in total, including one −$17,250 session. The result on Fed days comes from the event premium, not from selling volatility every day.

On timing, the far-OTM strangles had their highest win rates entering at 1:55pm (84% for the 16- and 10-delta), which captures the crush without holding through the morning. The ATM straddle did slightly better held from the open.

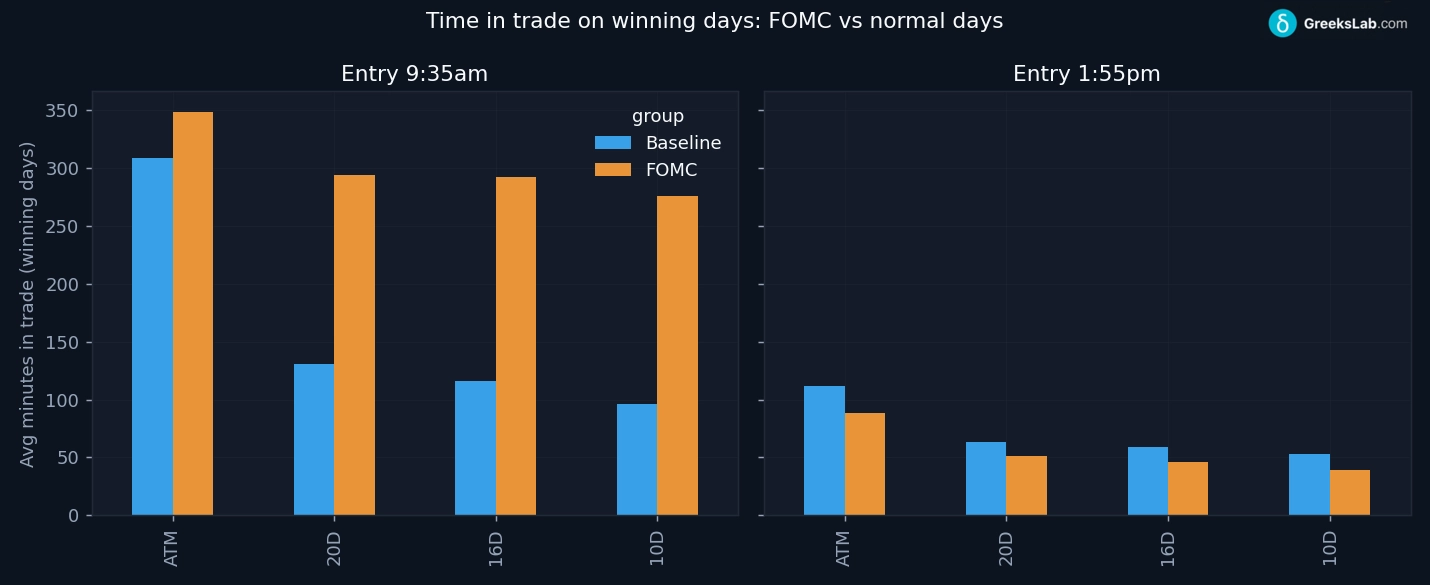

The 1:55pm entry doesn't just win often on Fed days — it wins quickly. Measuring the average time from entry to exit on profitable days makes the point.

A winning 1:55pm trade on a Fed day closed in about 39 to 88 minutes depending on the structure — that is, by roughly 2:35 to 3:25pm. The post-2:00pm crush drives the position to the 50% profit target almost immediately. A 9:35am entry, by contrast, sits for about five to six hours: it waits through the morning while premium is held flat, then only crushes at 2:00pm.

The same 1:55pm trade also closed faster on Fed days than on normal days — for example, a winning 16-delta strangle took about 46 minutes on a Fed day versus 59 on a normal one. The event crush accelerates the exit. For a seller who wants capital tied up for the shortest time, the 1:55pm Fed-day entry is the most efficient of the setups tested.

Create a free account or sign in to access: