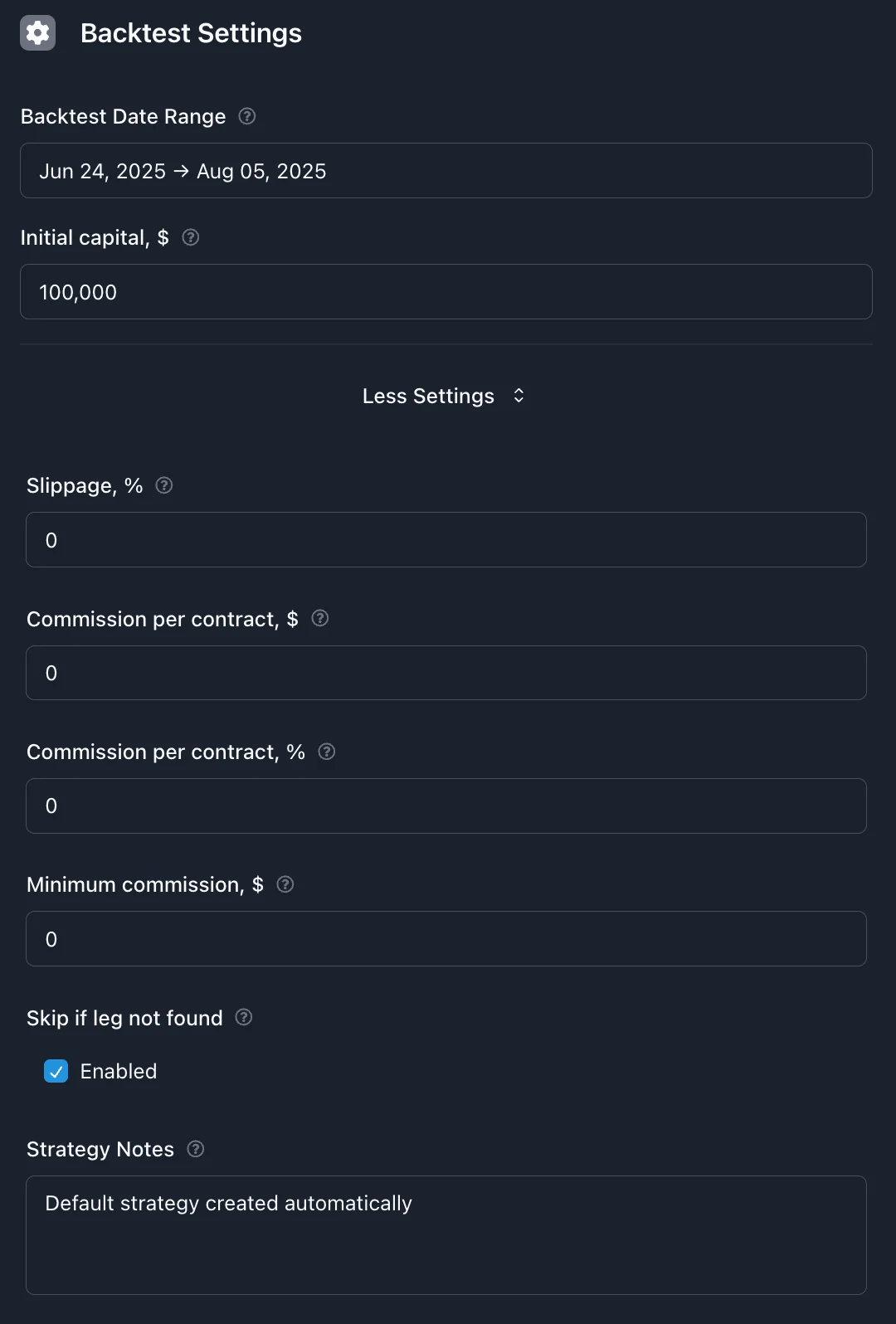

Configure backtest dates range, capital, transaction costs, and other simulation parameters

Backtest Settings

Set up your backtest to simulate how your strategy would have performed with real market data. These settings help make your backtest results as realistic as possible.

Testing Period

Choose the time period you want to test your strategy against. This is when your strategy will be "trading" in the simulation.

Quick Select Presets

Use the Quick Select dropdown to instantly set up common testing periods:

Recent Performance:

Last 7 days: Very short-term testing

Last 30 days: Recent month performance

Month to date: Current month so far

Year to date: Current year performance

Last 365 days: Rolling one-year period

Last 2 years: Two-year rolling window

Market Events & Conditions:

SPX Daily Expirations: Since May 2022 when daily SPX options launched

COVID Crash: Feb 20 - Mar 23, 2020 (market crash period)

2020-2021 Bull Market: Mar 24, 2020 - Dec 31, 2021 (recovery period)

Meme Stock Frenzy: January 2021 (GME/AMC volatility)

Volmageddon: Jan 26 - Feb 28, 2018

💡 Tip:

Try testing your strategy across different market events to see how it handles various conditions. The preset periods make it easy to test specific scenarios.

How Long Should You Test?

3-6 Months: Quick Testing

Good for: Testing new ideas quickly

Benefits: Fast results, easy to iterate

Limitation: May miss seasonal patterns

1-2 Years: Standard Testing

Good for: Most strategies

Benefits: Captures different market conditions

Recommended: Best balance of thoroughness and speed

3+ Years: Comprehensive Testing

Good for: Final validation before live trading

Benefits: Multiple market cycles and volatility periods

Limitation: Takes longer to run

⚠️ Important:

Include both calm and volatile periods in your test to see how your strategy handles different market conditions.

Starting Capital

Set the amount of money your virtual account starts with. This determines how many contracts you can trade and affects your percentage returns.

💡 Tip:

Use an amount close to what you'd actually trade with. This makes your backtest results more meaningful for real trading decisions.

Trading Costs

Add realistic trading fees to see how they affect your strategy's profitability. Most brokers charge a fee for each options contract you trade.

Commission Per Contract

This is how much your broker charges for each options contract you buy or sell.

Common Broker Fees:

Robinhood, Webull: $0.00 (commission-free)

TD Ameritrade, E*TRADE: $0.65 per contract

Interactive Brokers: $0.65 per contract (but lower for high volume)

Traditional Full-Service: 1.00−3.00+ per contract

💡 Example:

Iron Condor Trade (4 legs, 1 contract each):

Open position: 4 contracts × $0.65 = $2.60

Close position: 4 contracts × $0.65 = $2.60

Total cost: $5.20 in commissions

⚠️ Important:

Even small commission fees can significantly impact short-term strategies or strategies with frequent trading.

Slippage

Slippage accounts for the reality that you rarely get the exact mid-market price when trading. It represents the cost of crossing the bid-ask spread and market impact.

What Slippage Means

When you see an option quoted at $2.00, that might be the mid-price between a $1.95 bid and $2.05 ask. In reality:

Buying: You'll probably pay closer to $2.05 (or higher)

Selling: You'll probably receive closer to $1.95 (or lower)

Slippage simulates this real-world trading cost as a percentage of the option premium.

Recommended Slippage Settings

0% - Perfect World

Assumes you always get mid-market prices

Unrealistic but useful to see best-case performance

1-2% - Typical Retail Trader

Realistic for most individual traders

Recommended starting point: 1.5%

3-5% - Conservative Estimate

Accounts for poor market conditions or wide spreads

Good for stress testing your strategy

💡 Example:

Iron Condor selling for $300 premium with 2% slippage:

Perfect execution: Collect $300

With slippage: Actually collect $294 ($6 less)

When closing at 50% profit target: Pay $153 instead of $150

Additional Settings

Skip Missing Options

Recommended: Keep this ON

When your strategy looks for specific options (like a 16-delta put), sometimes those exact options don't exist in the historical data. With this setting enabled:

ON: Skip the trade entirely if any leg is missing (recommended)

OFF: Open whatever legs are available (can create unintended positions)

⚠️ Important:

Keeping this ON ensures your backtests only include the exact strategies you intended to test.

Quick Setup Guide

For Most Strategies

Good starting settings that work for most people:

Testing Period: 1-2 years of recent data

Starting Capital: $50,000 (or close to what you'd actually use)

Commission: Your broker's actual rate (check their website)

Slippage: 1.5%

Skip Missing Options: ON

Testing Different Market Conditions

Try these periods to see how your strategy handles different markets:

Bull Market: January 2017 - January 2020

Bear Market: January 2022 - December 2022 High Volatility: March 2020 - December 2020

Low Volatility: January 2017 - December 2017

Common Mistakes to Avoid

Don't use unrealistic settings like 0% commission and 0% slippage. Your backtest will look too good and disappoint in real trading.

Using perfect execution costs: Real trading has costs

Testing only good markets: Include volatile and down periods

Wrong position sizes: Match your actual trading capital

Next Steps

Once you've set up your backtest parameters, you're ready to run your test and analyze the results to see how your strategy performed.